Accidents happen, but Florida law doesn’t make it easy to recover what you are owed if you’re the victim of a preventable accident due to the negligence of another driver. Because Florida is a no-fault state, there are limits to when and how you can sue another person for an accident, plus requirements for car insurance.

Let’s break down what Florida’s no-fault car insurance law means, how it affects lawsuit liability, and more.

Florida Is a “No-Fault” State – What Does it Mean?

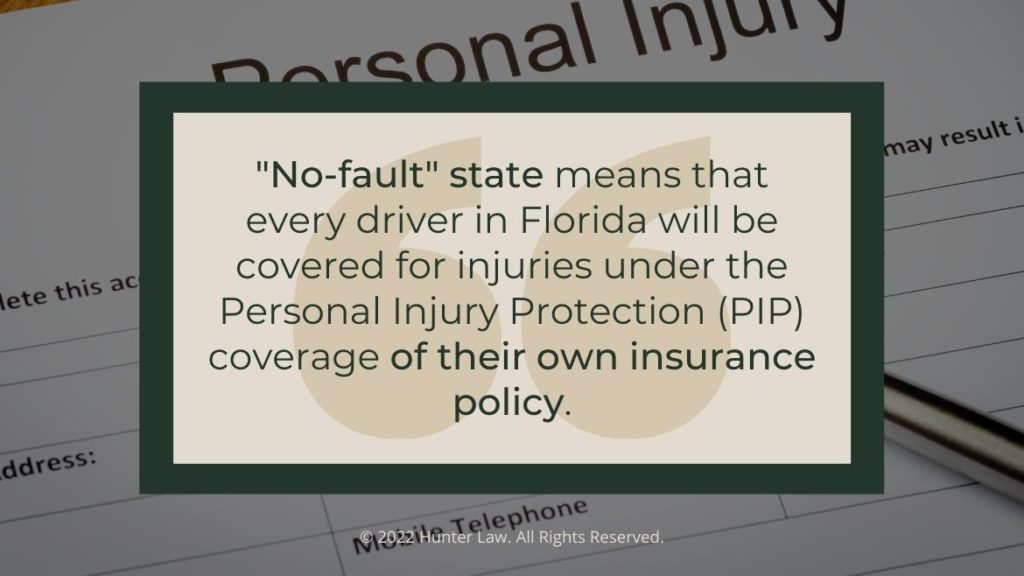

Florida, alongside 11 other states in the US, is a “no-fault” state. This term is a bit of a misnomer and can cause some confusion. It doesn’t specifically concern who is at fault for an accident, but rather means that every driver in Florida will be covered for injuries under the Personal Injury Protection (PIP) coverage of their own insurance policy.

No-fault laws were enacted in the 1970s in an attempt to lower insurance premiums for drivers and streamline the damages recovery process. However, this has gradually made things more complex and frustrating for responsible drivers over the years.

If two Florida drivers are involved in a car accident and are injured, both file a claim with their separate insurance companies. The insurance companies then pay for a percentage of their own insured’s medical bills up to a maximum of $10,000.

Does Everyone Have to Have Personal Injury Protection Insurance?

Yes. Florida, as a “no-fault” state requires that every legal driver have both:

- $10,000 in Property Damage Liability (PDL) benefits, which apply if you damage the property or vehicle of another person

- $10,000 in Personal Injury Protection (PIP) insurance, which applies to any injuries that you may sustain in an accident

On the other hand, drivers are not required to carry liability coverage for any injuries suffered by other drivers, passengers, bicyclists, or pedestrians. In this way, every individual driver in Florida is responsible for their own insurance coverage.

What Does PIP Insurance Cover?

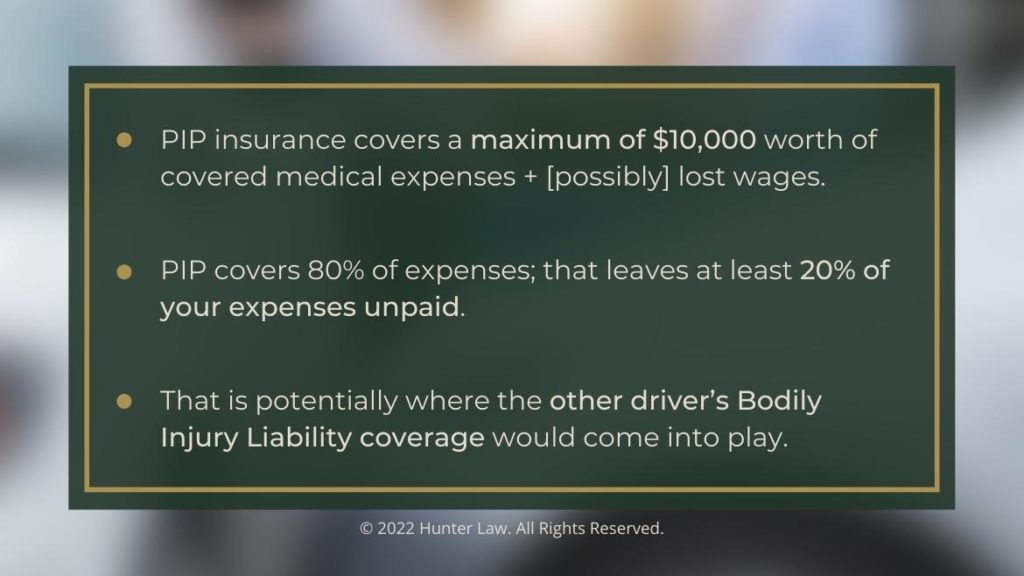

As noted, PIP insurance covers a maximum of $10,000 worth of covered medical expenses and, if your policy allows, lost wages. The medical expenses are calculated by taking the Medicare fee schedule and multiplying it by 2. For example, if Medicare would normally pay $50 for a medical charge, the doctor could bill a maximum of $100 under your PIP insurance coverage. From there, your insurance company would pay 80% of that amount, in this case, $80, leaving a $20 balance. Additionally, some PIP insurance policies carry a deductible of up to $1,000, meaning the first $1,000 of your medical expenses would not be covered by your PIP benefits.

If your policy carries wage loss coverage, you could also receive 60% of your lost wages to cover the time that the accident forced you to miss work. However, the most that your PIP coverage will pay combined between your medical expenses and lost wages is $10,000.

With PIP only covering 80% of the medical expenses it still leaves at least 20% of your medical expenses unpaid. That is potentially where the other driver’s Bodily Injury Liability coverage would come into play.

Pursuing Damages Against the Other Driver

If the other driver was at-fault for causing the accident, they would be responsible for at least the 20% in medical expenses that your PIP does not pay. If your injuries are significant enough and are deemed to be “a permanent injury” by your medical providers, then the at-fault driver would be responsible for not only the 20% that PIP does not cover and your PIP deductible if any, but also for 100% of any past medical treatment and lost wages that exceed the $10,000 PIP maximum payout, your pain, and suffering and, potentially, any future economic damages that you may incur.

If the driver that caused the accident carried Bodily Injury Liability coverage, then you would be able to present a claim against them to their insurance company in order to recover the full value of your damages.

How Legal Advisors Can Help

Presenting a claim to the at-fault driver’s insurance carrier can be a daunting task, especially if you don’t have the knowledge and training in knowing what damages you are entitled to recover. That is where having an experienced and knowledgeable personal injury attorney on your side to fight for you and your rights comes into play. Your lawyer will have legal knowledge of Florida’s “no-fault” insurance law to effectively handle your claim. Also, if the insurance carrier doesn’t handle your claim fairly, your lawyer should be able to advise you as such and file a lawsuit on your behalf. Having a skilled and knowledgeable attorney working for you is the best way to hold the insurance carriers accountable and to make certain that you are receiving a fair settlement for your case.

If you have been injured in a car accident and are wondering about your next step, contact Hunter Law today. As experienced Tampa personal injury lawyers, we can advise you about every aspect of your claim and make certain that you are being treated fairly and with integrity and, if you aren’t, sue those responsible for causing your injuries.

Still have more questions about the Florida “no-fault” insurance law? Contact us today for a free consultation and more information.